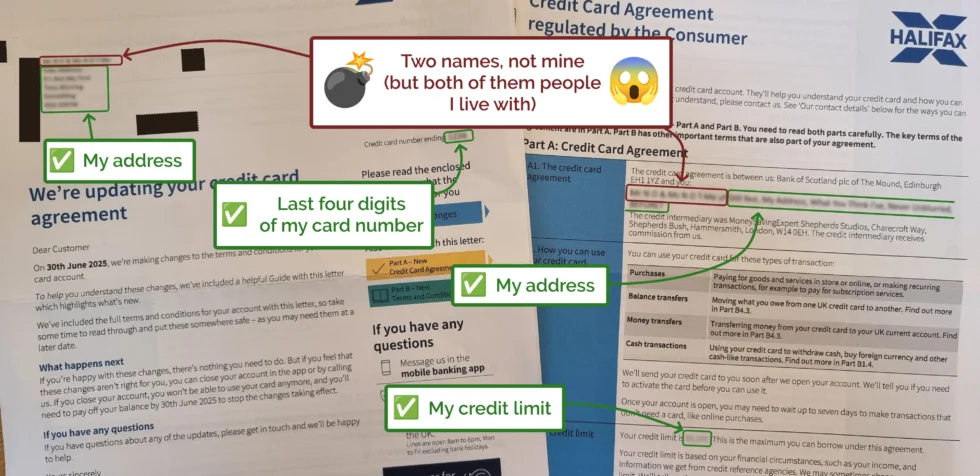

Today, Ruth and JTA received a letter. It told them about an upcoming change to the

agreement of their (shared, presumably) Halifax credit card.

Except… they don’t have a shared Halifax credit card. Could it be a scam? Some sort of phishing attempt, maybe, or perhaps somebody taking out a credit card in their names?

I happened to be in earshot and asked to take a look at the letter, and was surprised to discover that all of the other details – the last four digits of the card, the credit

limit, etc. – all matched my Halifax credit card.

Halifax sent a letter to me, about my credit card… but addressed it to… two other people I live with‽

I spent a little over half an hour on the phone with Halifax, speaking to two different advisors, who couldn’t fathom what had happened or how. My credit card is not (and has never

been) a joint credit card, and the only financial connection I have to Ruth and JTA is that I share a mortgage with them. My guess is that some person or computer at Halifax tried to

join-the-dots from the mortgage outwards and re-assigned my credit card to them, instead?

Eventually I had to leave to run an errand, so I gave up on the phone call and raised a complaint with Halifax in writing. They’ve promised to respond within… eight weeks. Just

brilliant.

It’s always been a bit of an inconvenience to have to do these things, but it’s never been a terrible burden: even when I fly internationally – which is probably the hardest

part of having my name – I’ve learned the tricks I need to minimise how often I’m selected for an excessive amount of unwanted “special treatment”.

I plan to make my first trip to the USA since my name change, next year. Place bets now on how that’ll go.

This year, though, for the very first time, my (stupid bloody) unusual name paid for itself. And not just in the trivial ways I’m used to, like being able to spot my badge instantly on

the registration table at conferences I go to or being able to fill out paper forms way faster than normal people. I mean in a concrete, financially-measurable way. Wanna hear?

So: I’ve a routine of checking my credit report with the major credit reference agencies every few years. I’ve been doing so since long before doing so became free (thanks GDPR); long even before

I changed my name: it just feels like good personal data housekeeping, and it’s interesting to see what shows up.

It started out with the electoral roll. How did it end up like this? It was only the electoral roll. It was only the electoral roll.

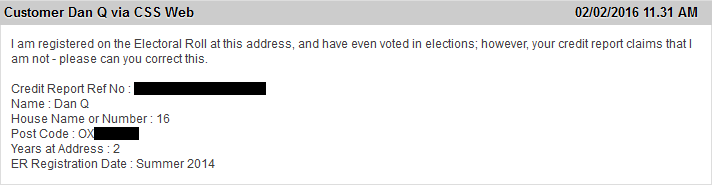

And so I noticed that my credit report with Equifax said that I wasn’t on the electoral roll. Which I clearly am. Given that my credit report’s pretty glowing, I wasn’t too worried, but

I thought I’d drop them an email and ask them to get it fixed: after all, sometimes lenders take this kind of thing into account. I wasn’t in any hurry, but then, it seems: neither were

they –

2 February 2016 – I originally contacted them

18 February 2016 – they emailed to say that they were looking into it and that it was taking a while

22 February 2016 – they emailed to say that they were still looking into it

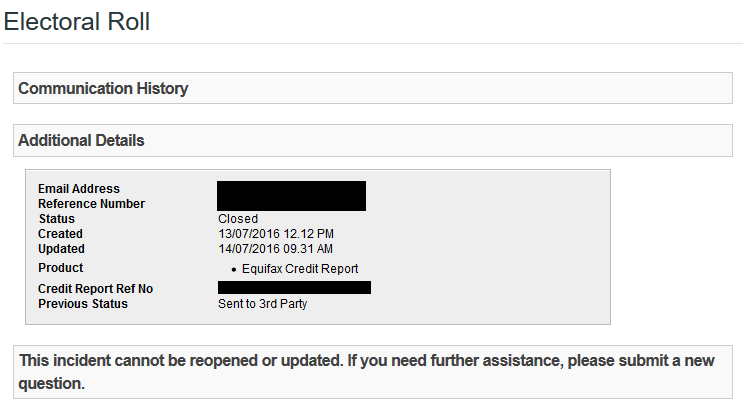

13 July 2016 – they emailed to say that they were still looking into it (which was a bit of a surprise, because after so long I’d almost forgotten that I’d even asked)

14 July 2016 – they marked the issue as “closed”… wait, what?

Given that all they’d done for six months was email me occasionally to say that it was taking a while, it was a little insulting to then be told they’d solved it.

I wasn’t in a hurry, and 2017 was a bit of a crazy year for me (for Equifax too, as it happens), so I ignored it for a bit, and

then picked up the trail right after the GDPR came into force. After all, they were storing personal information

about me which was demonstrably incorrect and, continued to store and process it even after they’d been told that it was incorrect (it’d have been a violation of principle 4 of the DPA 1998, too, but the GDPR‘s got bigger teeth: if you’re going to sick the law on somebody, it’s better that it has bark and bite).

Throwing the book tip-of-the-day: don’t threaten, just explain what you require and under what legal basis you’re able to do so. Let lawyers do the tough stuff.

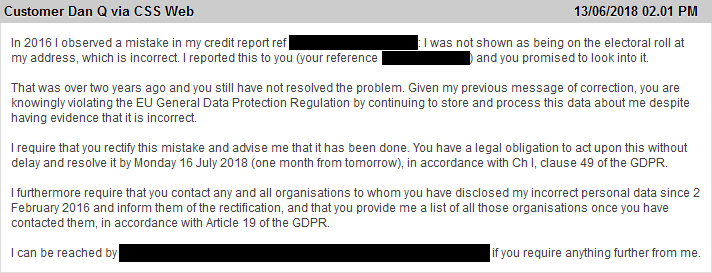

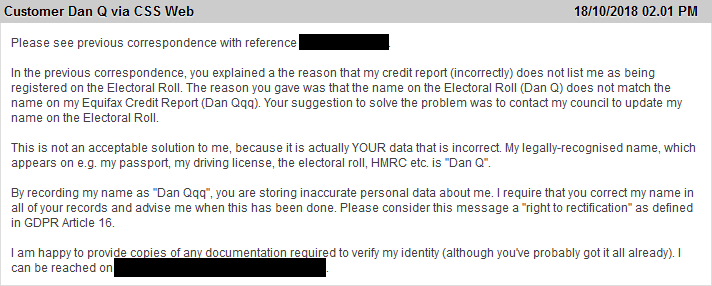

My anticipation was that my message of 13 July 2018 would get them to sit up and fix the issue. I’d assumed that it was probably related to my unusual name and that bugs in

their software were preventing them from joining-the-dots between my credit report and the Electoral Roll. I’d also assumed that this nudge would have them either fix their software… or

failing that, manually fix my data: that can’t be too hard, can it?

Apparently it can:

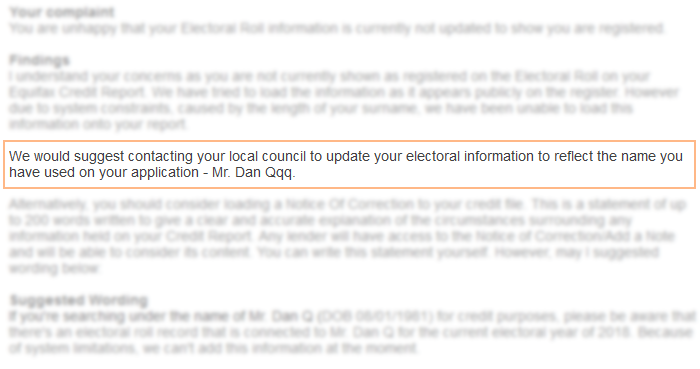

You want me to make it my problem, Equifax, and you want me to change my name on the Electoral Roll to match the incorrect name you use to refer to me in your systems?

Equifax’s suggested solution to the problem on my credit report? Change my name on the Electoral Roll to match the (incorrect) name they store in their systems (to work around

a limitation that prevents them from entering single-character surnames)!

At this point, they turned my send-a-complaint-once-every-few-years project into a a full blown rage. It’s one thing if you need me to be understanding of the time it can take to fix

the problems in your computer systems – I routinely develop software for large and bureaucratic organisations, I know the drill! – but telling me that your bugs are my problems

and telling me that I should lie to the government to work around them definitely isn’t okay.

Dear Equifax: No. No no no. No. Also, no. Now try again. Love Dan.

At this point, I was still expecting them to just fix the problem: if not the underlying technical issue then instead just hack a correction into my report. But clearly they considered

this, worked out what it’d cost them to do so, and decided that it was probably cheaper to negotiate with me to pay me to go away.

Which it was.

This week, I accepted a three-figure sum from Equifax as compensation for the inconvenience of the problem with my credit report (which now also has a note of correction, not that my

alleged absence from the Electoral Roll has ever caused my otherwise-fine report any trouble in the past anyway). Curiously, they didn’t attach any strings to the deal, such as not

courting publicity, so it’s perfectly okay for me to tell you about the experience. Maybe you know somebody who’s similarly afflicted: that their “unusual” name means that a

credit reference company can’t accurately report on all of their data. If so, perhaps you’d like to suggest that they take a look at their credit report too… just saying.

You can pay for me to go away, but it takes more for me to shut up. (A lesson my parents learned early on.)

Apparently Equifax think it’s cheaper to pay each individual they annoy than it is to fix their database problems. I’ll bet that, in the long run, that isn’t true. But in the meantime,

if they want to fund my recent trip to Cornwall, that’s fine by me.