I’m British. So I complain about very little. Instead, I tut loudly to myself.

But the thing that makes me tut the loudest, perhaps, is when I discover that somebody has put a roll of toilet paper on its holder the wrong way.

Of all the hills a person could choose to die on, I seem to have chosen the most absorbent.

I’m aware that there are some people who do not hold a strong opinion on the correct orientation of a horizontally-mounted roll of toilet paper. That’s fine; not everybody has to care

about these things. Maybe you’ll be persuaded that there’s a “right” way by this post (and there is), but if not, no problem.

But for the anybody who deliberately and consciously hangs toilet paper the wrong way… here’s why you’re mistaken:

Hanging it the right way puts the loose end closer to the user, which means they’ve got less-far to reach.

Hanging it the right way means the loose end is easier to find, which is especially useful if you didn’t turn the light on yet because you’re not ready to fully

wake up.

Hanging it the wrong way increases the amount of time the paper spends cleaning the wall, which isn’t something I want or need it to be used to clean.

Hanging it the wrong way increases the risk that the loose end is in a place where it is inaccessible, sandwiched directly behind the roll and against the wall, requiring the user

to manually turn the roll to expose it. When the same thing happens on a roll hung the right way (which is rarer on account of gravity) a pinched end self-corrects as

soon as you pull the roll slightly away from the wall.

It’s been argued that your way is “tidier” because unused toilet paper sits closer to the wall which which it’s approximately parallel. Sure (although I disagree that it’s tidier,

but that’s clearly subjective): but I counter that I don’t need it to be tidy, I need it to function.

I’m willing to concede that for some pet owners and parents, hanging the “wrong” way might discourage curious animals and toddlers from playing with the exposed end. But even that’s

not a guarantee, as wrong-way-hanger Dan4th Nicholas discovered. Photo used under a CC-BY license.

I share a home with a wrong-way hanger, but about 13 years ago we came to a household agreement: I’d quietly “correct” any

incorrectly-installed toilet rolls in shared bathrooms1, and nobody would deliberately switch them back2,

and in exchange I’d refrain from trying to educate people about why they were wrong.3

Like Mike Wozniak, I also have a pet hate for people leaving the cardboard tube from toilet paper rolls in suboptimal places,

like on top of a closed pedal bin. But I don’t see so much of that.

1 A man can do whatever the hell he likes in the comfort of his own en suite.

2 This clause was added after it became apparent that our then-housemate Paul decided it’d be a fun prank to go around the house reversing my corrections (not because he preferred the wrong way, but just to troll

me!). Which I can admit was a fun prank… until I challenged him on it and he denied it, at which point it became gaslighting.

3 This doesn’t count as forcing an education on my household. My blog isn’t in your face:

you can skip it any time you want. You can even lie and say you read it when you don’t; I won’t know, especially this month when I’ve been writing so prolifically – now on my longest-ever daily streak! – that I probably won’t even remember what I wrote about.

Our household costs have increased considerably over the last decade, not least because children and pets are expensive (who knew?).

Sample data

For my examples below, assume a three-person family. I’m using unrealistic numbers for easy arithmetic.

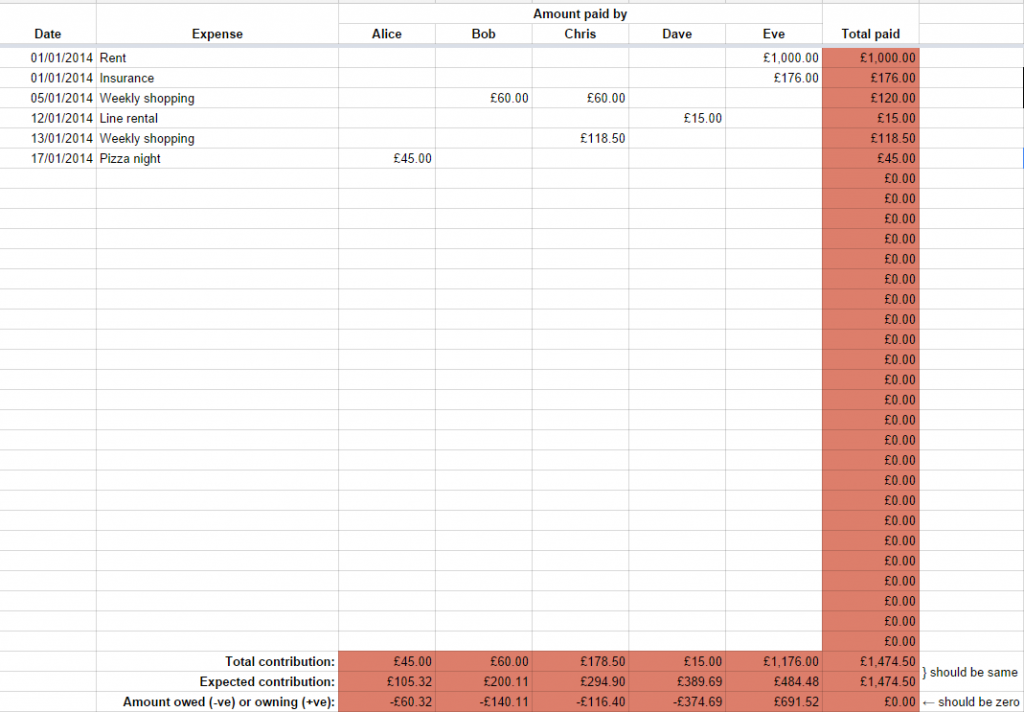

Alice earns £2,000, Bob earns £1,000, and Chris earns £500, for a total household income of £3,500.

Alice spends £1,450, Bob £800, and Chris £250, for a total household expenditure of £2,500.

Model #1: Straight Split

We’ve never done things this way, but for completeness sake I’ll mention it: the simplest way that households can split their costs is by dividing them between the participants equally:

if the family make a £60 shopping trip, £20 should be paid by each of Alice, Bob, and Chris.

My example above shows exactly why this might not be a smart choice: this model would have each participant contribute £833.33 over the course of the month, which is more than Chris

earned. If this month is representative, then Chris will gradually burn through their savings and go broke, while Alice will put over a grand into her savings account every month!

“Land, Bread, Peace… and Spreadsheets!”

Model #2: Income-Assessed

We’re a bunch of leftie socialist types, and wanted to reflect our political outlook in our household finances, too. So rather than just splitting our costs equally between us, we

initially implemented a means-assessment system based on the relative differences between our incomes. The thinking was that somebody that earns twice as much should

contribute twice as much towards the costs of running the household.

Using our example family above, here’s how that might look:

Alice earned 57% of the household income, so she should have contributed 57% of the household costs: £1,425. She overpaid by £25.

Bob earned 29% of the household income, so he should have contributed 29% of the household costs: £725. He overpaid by £75.

Chris earned 14% of the household income, so they should have contributed 14% of the household costs: £350. They underpaid by £100.

Therefore, at the end of the month Chris should settle up by giving £25 to Alice and £75 to Bob.

By analogy: The “Income-Assessed” model is functionally equivalent to splitting each and every expense according to the participants income – e.g. if a £100 bill landed

on their doormat, Alice would pay £57, Bob £29, and Chris £14 of it – but has the convenience that everybody just pays for things “as they go along” and then square everything up when

their paycheques come in.

You know what else is surprisingly expensive? Having the roof of your house taken off.

Over time, our expenditures grew and changed and our incomes grew, but they didn’t do so in an entirely simple fashion, and we needed to make some tweaks to our income-assessed model of

household finance contributions. For example:

Gross vs Net Income: For a while, some of our incomes were split into a mixture of employed income (on which income tax was paid as-we-earned) and self-employed

income (for which income tax would be calculated later), making things challenging. We agreed that net income (i.e. take-home pay) was the correct measure for us to use for the

income-based part of the calculation, which also helped keep things fair as some of us began to cross into and out of the higher earner tax bracket.

Personal Threshold: At times, a subset of us earned a disproportionate portion of the household income (there were short periods where one of us earned over 50% of

the household income; at several other times two family members each earned thrice that of the third). Our costs increased too, but this imposed an regressive burden on the

lower-earner(s), for whom those costs represented a greater proportion of their total income. To attempt to mitigate this, we introduced a personal threshold somewhat analogous to the

income tax “personal allowance” (the policy that means that you don’t pay tax on your first £12,570 of income).

Eventually, we came to see that what we were doing was trying to patch a partially-broken system, and tried something new!

Model #3: Same-Residual

In 2022, we transitioned to a same-residual system that attempts to share out out money in an even-more egalitarian way. Instead of each person contributing in accordance

with their income, the model attempts to leave each person with the same average amount of disposable personal income at the end. The difference is most-profound where the

relative incomes are most-diverse.

With the example family above, that would mean:

The household earned £3,500 and spent £2,500, leaving £1,000. Dividing by 3 tells us that each person should have £333.33 after settling up.

Alice earned earned £2,000 and spent £1,450, so she has £550 left. That’s £216.67 too much.

Bob earned earned £1,000 and spent £800, so she has £200 left. That’s £133.33 too little.

Chris earned earned £500 and spent £250, so she has £250 left. That’s £83.33 too little.

Therefore, at the end of the month Alice should settle up by giving £133.33 to Bob and £83.33 to Chris (note there’s a 1p rounding error).

That’s a very different result than the Income-Assessed calculation came up with for the same family! Instead of Chris giving money to Alice and Bob, because those two

contributed to household costs disproportionately highly for their relative incomes, Alice gives money to Bob and Chris, because their incomes (and expenditures) were much lower.

Ignoring any non-household costs, all three would expect to have the same bank balance at the start of the month as at the end, after settlement.

By analogy: The “Same-Residual” model is functionally equivalent to having everybody’s salary paid into a shared bank account, out of which all household expenditures

are paid, and at the end of the month everything that’s left in the bank account gets split equally between the participants.

Our version of the spreadsheet has inherited a lot of hacky edges, many for now-unused functionality.

We’ve made tweaks to this model, too, of course. For example: we’ve set a “target” residual and, where we spend little enough in a month that we would each be eligible for more

than that, we instead sweep the excess into our family savings account. It’s a nice approach to help build up a savings reserve without feeling a pinch.

I’m sure our model will continue to evolve, as it has for the last decade and a half, but for now it seems stable, fair, and reasonable. Maybe it’ll work for your household too (whether

or not you’re also a polyamorous family!): take a look at the spreadsheet in Google Drive and give it a go.

For the last four years or so, Ruth, JTA and I (and

during their times living with us, Paul and Matt) have organised our finances according to a system of means-assessment. I’ve mentioned it to people on a number of ocassions, and every time it seems to

attract interest, so I thought I’d explain how we got to it and how it works, so that others might benefit from it. We think it’s particularly good for families consisting of multiple

adults sharing a single household (for example, polyamorous networks like ours, or families with grown children) but there are probably others who’d benefit from it, too – it’s

perfectly reasonable for just two adults with different salaries to use it, for example. And I’ve made a

sample spreadsheet that you’re welcome to copy and adapt, if you’d like to.

How we got here

That’s a long receipt!

After I left Aberystwyth and Ruth, JTA, Paul and I started living at “Earth”, our

house in Headington, we realised that for the first time, the four of us were financially-connected to one another. We started by dividing the rent and council tax four ways (with an

exemption for Paul while he was still looking for work), splitting the major annual expenses (insurance, TV license) between the largest earners, and taking turns to pay smaller,

more-regular expenses (shopping, bills, etc.). This didn’t work out very well, because it only takes two cycles of you being the “unlucky” one who gets lumbered with the

more-expensive-than-usual shopping trip – right before a party, for example – before it starts to feel like a bit of a lottery.

Our solution, then, was to replace the system with a fairer one. We started adding up our total expenditures over the course of each month and settling the difference between one

another at the end of each month. Because we’re clearly raging socialists, we decided that the fairest (and most “family-like”) way to distribute responsibility was by a system of

partial means-assessment: de chacun selon ses facultés.

Another enormous shopping trip.

We started out with what we called “75% means-assessment”: in other words, a quarter of our shared expenditures were split evenly, four ways, and three-quarters were split

proportionally in accordance with our gross income. We arrived at that figure after a little dissussion (and a computerised model that we could all play with on a big screen). Working

from gross income invariably introduces inequalities into the system (some of which are mirrored in our income tax system) but a bigger unfairness came – as it does in wider society –

from the fact that the difference between a very-low income and a low income is significantly more (from a disposable money perspective) than the difference between a low and a high

income. This was relevant, because ‘personal’ expenses, such as mobile phone bills, were not included in the scheme and so we may have penalised lower-earners more than we had intended.

On the other hand, 75% means-assessment was still significantly more-“communist” than 0%!

When I mentioned this system to people, sometimes they’d express surprise that I (as one of the higher earners) would agree to such an arrangement: the question was usually asked with a

tone that implied that they expected the lower earners to mooch off of the higher earners, which (coupled with the clearly false idea that there’s a linear relationship between the

amount of work involved in a job and the amount that it pays) would result in a “race to the bottom”, with each participant trying to do the smallest amount of work possible in order to

maximise the degree to which they were subsidised by the others. From a game theory perspective, the argument makes sense, I would concede. But on the other hand – what the hell would I

be doing agreeing to live with and share finances with (and then continuing to live with and share finances with) people whose ideology was so opposed to my own in the first place?

Naturally, I trusted my fellow Earthlings in this arrangement: I already trusted them – that’s why I was living with them!

Louis Blanc had the right idea, but his idealism was hampered by the selfishness inherent in any sufficiently-large group. Had he brought socialism to his house, rather than his

country, he might have felt more successful.

How it works

We’ve had a few iterations, but we eventually settled on a system at a higher rate of means-assessment: 100%! It’s not perfect, but it’s the fairest way I’ve ever been involved with of

sharing the costs of running a house. I’ve put together a spreadsheet based on the one that we use that you can adapt to your own household, if you’d like to try a fairer way of

splitting your bills – whether there are just two of you or lots of you in your home, this provides a genuinely equitable way to share your costs.

Click on the sheet to see a Google Drive document that you can save a copy of and adapt to your own household.

The sheet I’ve provided – linked above – is not quite like ours: ours has extra features to handle Ruth and I’s fluctuating income (mine because of freelance work, Ruth’s

because she’s gradually returning to work following a period

of maternity leave), an archive of each month’s finances, tools to help handle repayments to one another of money borrowed, and convenience macros to highlight who owes what to

whom. This is, then, a simplified version from which you can build a model for your own household, or that you can use as a starting point for discussions with your own tribe.

Start on the “People” sheet and tell it how many participants your household has, their names, and their relative incomes. Also add your proposed level of means-assessment: anything

from 0% to 100%… or beyond, but that does have some interesting philosophical consequences.

Then, on the “Expenses” sheet, record each thing that your household pays for over the course of each month. At the bottom, it’ll total up how much each person has paid, and how much

they would have been expected to pay, based on the level of your means-assessment: at 0%, for example, each person would be expected to pay 1/N

of the total; at the other extreme (100%), a person with no income would be expected to make no contribution, and a person with twice the income of another would be expected to pay

twice as much as them. It’ll also show the difference between the two values: so those who’ve paid less than their ‘share’ will have negative numbers and will owe money to those who’ve

paid more than their share, indicated by positive numbers. Settle the difference… and you’re ready to roll on to the next month.

Now you’re equipped to employ a (wholly or partially) means-assessed model to your household finances. If you adapt this model or have ideas for its future development, I’d love to hear

them.

Right now, Three Rings seems to be eating up virtually all of my time. It’s hardly the first time

– I complained about being incredibly busy

with Three Rings stuff just a couple of years ago, but somehow right now it’s busier than ever. There’s been the Milestone: Jethrik release, some complications with our uptime when our DNS servers

were hit by a DDoS attack, and – the big one – planning for this weekend’s conference.

Checking the timetable while I wait for inspiration to strike me about what to say about the “engagement” responsibilities of a Three Rings Administrator.

The Three Rings 10th Birthday Conference is this weekend, and I’ve somehow

volunteered myself to not only run the opening plenary but to run two presentations (one on the history of Three Rings, which I suppose I’m the best person to talk about, and one on

being an awesome Three Rings Administrator) and a problem-solving workshop. My mind’s been on overdrive for weeks, and I’m pretty sure I’m not even the one working the hardest (that

honour would have to go to poor JTA).

Still: all this work will pay off, I’m sure, and Saturday will be an event to remember. I’m looking forward to it… although right now I’d equally happily spend a week or two curled up

in bed under a blanket with a nice book and a mug of herbal tea, thanks.

In other news: Matt P‘s hanging out on Earth at the moment, (on his best behaviour I think) while Ruth, JTA and I decide if we’d like to live with him for a while. So far, I think he’s making a convincing argument. He’s proven

himself to be house trained (he hasn’t pooped on the carpet even once) and everything.

This morning I took a cycle out to the post office to put in the mail redirection forms (which they wouldn’t let us fill in online, and – in fact – they rejected once I got to the post

office because I’d used blue ink in one place on the form, rather than black… but that’s another story) in anticipation of the Earthlings‘ upcoming house move, and on my way out of the garage our neighbour came over.

“We’ll be sorry to see you go,” she said, gesturing at the “TO LET” sign at the end of the driveway.

“Hmm?” I responded. It took a while to sink in that she was talking to me: apart from an occasional “Hi” or “Bye” on the way in to or out of the house, we’ve never spoken to

one another before.

To Let sign outside Old Earth.

“Oh yeah,” I said, after a pause, “We’re moving over to the other side of the city: we kind-of wanted a bigger place for the four of us.”

“Oh,” she continued, “I suppose it might be a little small in there for four. It’s a shame, though: you’re the best tenants we’ve ever had.”

Something in my head snapped, and unraveled, and it took a little time before I managed to re-assemble her sentence into something that made sense to me.

“You… own this building?” I asked, pointing back at our house. We’d never met our landlords (at least, I thought we hadn’t): everything had always been arranged through our

letting agency.

There was another twang in my head as something else snapped. Then moments later, half way through my next thought, I realised how incredibly racist I was being. You see: our contract

had stated that our landlord’s name was Mr. Patel, and that’s a name that in my mind had associated itself with a certain tone of skin colour. And it had, for a moment, seemed

inconceivable that the plump white woman in front of me could possibly be part of the family of the imaginary Mr. Patel that had taken up residence in my head. As I worked to reprogram

my brain with this new information (and perhaps a little less capacity for runaway assumptions), she continued:

“The previous tenants have all been awful,” she said, “The last lot broke all of the windows. The ones before that tried to burn the place down!”

This actually went some way to explaining the state of the building, with it’s various weakened and damaged parts.

“Well thank you,” I said, “I hope you get some more great tenants next time.”

“Yeah,” she replied, “I was going to say that to your dad this morning when I saw him leaving.”

“My… dad?”

“Yeah: he left here earlier; just a bit before your girlfriend left. Sorry: is he not your father?”

Every string that still remaining intact in my brain snapped simultaneously. This woman had just blown my poor little mind. I investigated:

“Dark-haired chap, with a beard?” I queries, miming the shape of a beard because for some reason that made sense to me – you know, in case she’d never seen a beard before.

“Yeah, that’s him.”

“Wow. No, that’s JTA. He’s… like four years younger than me.”

“Oh God!” she said, “You can’t tell him I said that…”

But it was too late: the blog post was already half-written in my mind, taking up the void that had been cleared during the earlier series of mental implosions. This one’s for

you, pops.

My "father" updates the Earthlings' "Jump Track", a metaphor borrowed from the Battlestar Galactica board game to represent our readiness to "jump" to our new home. It looks like

moving now has a 25% chance of us leaving 3 people behind. Also, it looks like the Galactica has put on weight since it's last step.

My friend Kit already spends more of his life at my house than at his own. Today I found his electric shaver plugged in in my bathroom. I questioned him about it, and apparently I have

a suitable electrical outlet whereas he doesn’t, and this is the only reason, but I’m not so sure.

If he thinks he’s going to get to share my bed he has another thing coming.