My random Wikipedia article of the day was Milices Patriotiques, who were a 22,000-strong communist group and part of the Belgian resistance in the Second World War. Which sounded really interesting, but their article was tragically short so that’s pretty much all I have to say about them!

Tag: communism

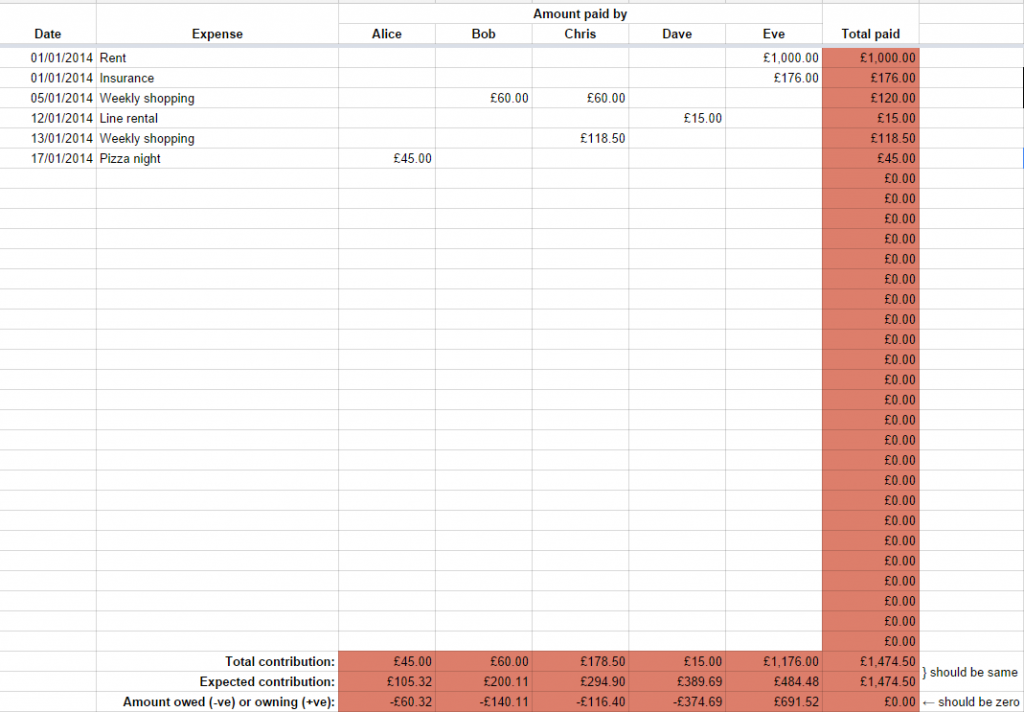

Household Finances Revisited

Almost a decade ago I shared a process that my domestic polyfamily and I had been using (by then, for around four years) to manage our household finances. That post isn’t really accurate any more, so it’s time for an update (there’s a link if you just want the updated spreadsheet):

Sample data

For my examples below, assume a three-person family. I’m using unrealistic numbers for easy arithmetic.

- Alice earns £2,000, Bob earns £1,000, and Chris earns £500, for a total household income of £3,500.

- Alice spends £1,450, Bob £800, and Chris £250, for a total household expenditure of £2,500.

Model #1: Straight Split

We’ve never done things this way, but for completeness sake I’ll mention it: the simplest way that households can split their costs is by dividing them between the participants equally: if the family make a £60 shopping trip, £20 should be paid by each of Alice, Bob, and Chris.

My example above shows exactly why this might not be a smart choice: this model would have each participant contribute £833.33 over the course of the month, which is more than Chris earned. If this month is representative, then Chris will gradually burn through their savings and go broke, while Alice will put over a grand into her savings account every month!

Model #2: Income-Assessed

We’re a bunch of leftie socialist types, and wanted to reflect our political outlook in our household finances, too. So rather than just splitting our costs equally between us, we initially implemented a means-assessment system based on the relative differences between our incomes. The thinking was that somebody that earns twice as much should contribute twice as much towards the costs of running the household.

Using our example family above, here’s how that might look:

- Alice earned 57% of the household income, so she should have contributed 57% of the household costs: £1,425. She overpaid by £25.

- Bob earned 29% of the household income, so he should have contributed 29% of the household costs: £725. He overpaid by £75.

- Chris earned 14% of the household income, so they should have contributed 14% of the household costs: £350. They underpaid by £100.

- Therefore, at the end of the month Chris should settle up by giving £25 to Alice and £75 to Bob.

By analogy: The “Income-Assessed” model is functionally equivalent to splitting each and every expense according to the participants income – e.g. if a £100 bill landed on their doormat, Alice would pay £57, Bob £29, and Chris £14 of it – but has the convenience that everybody just pays for things “as they go along” and then square everything up when their paycheques come in.

Over time, our expenditures grew and changed and our incomes grew, but they didn’t do so in an entirely simple fashion, and we needed to make some tweaks to our income-assessed model of household finance contributions. For example:

- Gross vs Net Income: For a while, some of our incomes were split into a mixture of employed income (on which income tax was paid as-we-earned) and self-employed income (for which income tax would be calculated later), making things challenging. We agreed that net income (i.e. take-home pay) was the correct measure for us to use for the income-based part of the calculation, which also helped keep things fair as some of us began to cross into and out of the higher earner tax bracket.

- Personal Threshold: At times, a subset of us earned a disproportionate portion of the household income (there were short periods where one of us earned over 50% of the household income; at several other times two family members each earned thrice that of the third). Our costs increased too, but this imposed an regressive burden on the lower-earner(s), for whom those costs represented a greater proportion of their total income. To attempt to mitigate this, we introduced a personal threshold somewhat analogous to the income tax “personal allowance” (the policy that means that you don’t pay tax on your first £12,570 of income).

Eventually, we came to see that what we were doing was trying to patch a partially-broken system, and tried something new!

Model #3: Same-Residual

In 2022, we transitioned to a same-residual system that attempts to share out out money in an even-more egalitarian way. Instead of each person contributing in accordance with their income, the model attempts to leave each person with the same average amount of disposable personal income at the end. The difference is most-profound where the relative incomes are most-diverse.

With the example family above, that would mean:

- The household earned £3,500 and spent £2,500, leaving £1,000. Dividing by 3 tells us that each person should have £333.33 after settling up.

- Alice earned earned £2,000 and spent £1,450, so she has £550 left. That’s £216.67 too much.

- Bob earned earned £1,000 and spent £800, so she has £200 left. That’s £133.33 too little.

- Chris earned earned £500 and spent £250, so she has £250 left. That’s £83.33 too little.

- Therefore, at the end of the month Alice should settle up by giving £133.33 to Bob and £83.33 to Chris (note there’s a 1p rounding error).

That’s a very different result than the Income-Assessed calculation came up with for the same family! Instead of Chris giving money to Alice and Bob, because those two contributed to household costs disproportionately highly for their relative incomes, Alice gives money to Bob and Chris, because their incomes (and expenditures) were much lower. Ignoring any non-household costs, all three would expect to have the same bank balance at the start of the month as at the end, after settlement.

By analogy: The “Same-Residual” model is functionally equivalent to having everybody’s salary paid into a shared bank account, out of which all household expenditures are paid, and at the end of the month everything that’s left in the bank account gets split equally between the participants.

We’ve made tweaks to this model, too, of course. For example: we’ve set a “target” residual and, where we spend little enough in a month that we would each be eligible for more than that, we instead sweep the excess into our family savings account. It’s a nice approach to help build up a savings reserve without feeling a pinch.

I’m sure our model will continue to evolve, as it has for the last decade and a half, but for now it seems stable, fair, and reasonable. Maybe it’ll work for your household too (whether or not you’re also a polyamorous family!): take a look at the spreadsheet in Google Drive and give it a go.

The last Soviet citizen: The cosmonaut who was left behind in space – Russia Beyond

This is a repost promoting content originally published elsewhere. See more things Dan's reposted.

Sergei Krikalev was in space when the Soviet Union collapsed. Unable to come home, he wound up spending two times longer than originally planned in orbit. They simply refused to bring him back.

Sergei Krikalev was in space when the Soviet Union collapsed. Unable to come home, he wound up spending two times longer than originally planned in orbit. They simply refused to bring him back.While tanks were rolling through Moscow’s Red Square, people built barricades on bridges, Mikhail Gorbachev and the Soviet Union went the way of history, Sergei Krikalev was in space. 350 km away from Earth, the Mir space station was his temporary home.

He was nicknamed “the last citizen of the USSR.” When the Soviet Union broke apart into 15 separate states in 1991, Krikalev was told that he could not return home because the country that had promised to bring him back home no longer existed.

…

Diary

This is a repost promoting content originally published elsewhere. See more things Dan's reposted.

The time capsule was buried in a secluded square in Murmansk in 1967 on the eve of the fiftieth anniversary of the Russian Revolution. Inside was a message dedicated to the citizens of the Communist future. At short notice, the authorities brought forward the capsule’s exhumation by ten days, to coincide with the city’s 101st birthday. With the stroke of an official’s pen, a mid-century Soviet relic was enlisted to honour one of the last acts of Tsar (now Saint) Nicholas II, who founded my hometown in October 1916. From socialism to monarchism in ten days. Some of the city’s pensioners accused the local government of trying to suppress the sacred memory of the revolution. ‘Our forefathers would be turning in their graves,’ one woman wrote in a letter to the local paper. The time capsule ‘is not some kind of birthday present to the city; it’s a reminder of the centenary of the great October Revolution and its human cost.’

My father had watched the time capsule being buried. He came to Murmansk aged 17. From his remote village, he had dreamed of the sea but he failed the navy’s eye test. In October 1967, he was a second-year student at the Higher Marine Engineering Academy, an elite training school for the Soviet Union’s massive fishing fleet. As a year-round warm water port, Murmansk – the largest human settlement above the Arctic Circle – is a major fishing and shipping hub, home to the world’s only fleet of nuclear-powered ice-breakers…

Means-Assessed Household Finances (Socialism Begins At Home!)

In 2023 I published an updated version of this blog post. See that post for the latest tips on managing polyfamily finances in a socialist manner.

For the last four years or so, Ruth, JTA and I (and during their times living with us, Paul and Matt) have organised our finances according to a system of means-assessment. I’ve mentioned it to people on a number of ocassions, and every time it seems to attract interest, so I thought I’d explain how we got to it and how it works, so that others might benefit from it. We think it’s particularly good for families consisting of multiple adults sharing a single household (for example, polyamorous networks like ours, or families with grown children) but there are probably others who’d benefit from it, too – it’s perfectly reasonable for just two adults with different salaries to use it, for example. And I’ve made a sample spreadsheet that you’re welcome to copy and adapt, if you’d like to.

How we got here

After I left Aberystwyth and Ruth, JTA, Paul and I started living at “Earth”, our house in Headington, we realised that for the first time, the four of us were financially-connected to one another. We started by dividing the rent and council tax four ways (with an exemption for Paul while he was still looking for work), splitting the major annual expenses (insurance, TV license) between the largest earners, and taking turns to pay smaller, more-regular expenses (shopping, bills, etc.). This didn’t work out very well, because it only takes two cycles of you being the “unlucky” one who gets lumbered with the more-expensive-than-usual shopping trip – right before a party, for example – before it starts to feel like a bit of a lottery.

Our solution, then, was to replace the system with a fairer one. We started adding up our total expenditures over the course of each month and settling the difference between one another at the end of each month. Because we’re clearly raging socialists, we decided that the fairest (and most “family-like”) way to distribute responsibility was by a system of partial means-assessment: de chacun selon ses facultés.

We started out with what we called “75% means-assessment”: in other words, a quarter of our shared expenditures were split evenly, four ways, and three-quarters were split proportionally in accordance with our gross income. We arrived at that figure after a little dissussion (and a computerised model that we could all play with on a big screen). Working from gross income invariably introduces inequalities into the system (some of which are mirrored in our income tax system) but a bigger unfairness came – as it does in wider society – from the fact that the difference between a very-low income and a low income is significantly more (from a disposable money perspective) than the difference between a low and a high income. This was relevant, because ‘personal’ expenses, such as mobile phone bills, were not included in the scheme and so we may have penalised lower-earners more than we had intended. On the other hand, 75% means-assessment was still significantly more-“communist” than 0%!

When I mentioned this system to people, sometimes they’d express surprise that I (as one of the higher earners) would agree to such an arrangement: the question was usually asked with a tone that implied that they expected the lower earners to mooch off of the higher earners, which (coupled with the clearly false idea that there’s a linear relationship between the amount of work involved in a job and the amount that it pays) would result in a “race to the bottom”, with each participant trying to do the smallest amount of work possible in order to maximise the degree to which they were subsidised by the others. From a game theory perspective, the argument makes sense, I would concede. But on the other hand – what the hell would I be doing agreeing to live with and share finances with (and then continuing to live with and share finances with) people whose ideology was so opposed to my own in the first place? Naturally, I trusted my fellow Earthlings in this arrangement: I already trusted them – that’s why I was living with them!

How it works

We’ve had a few iterations, but we eventually settled on a system at a higher rate of means-assessment: 100%! It’s not perfect, but it’s the fairest way I’ve ever been involved with of sharing the costs of running a house. I’ve put together a spreadsheet based on the one that we use that you can adapt to your own household, if you’d like to try a fairer way of splitting your bills – whether there are just two of you or lots of you in your home, this provides a genuinely equitable way to share your costs.

The sheet I’ve provided – linked above – is not quite like ours: ours has extra features to handle Ruth and I’s fluctuating income (mine because of freelance work, Ruth’s because she’s gradually returning to work following a period of maternity leave), an archive of each month’s finances, tools to help handle repayments to one another of money borrowed, and convenience macros to highlight who owes what to whom. This is, then, a simplified version from which you can build a model for your own household, or that you can use as a starting point for discussions with your own tribe.

Start on the “People” sheet and tell it how many participants your household has, their names, and their relative incomes. Also add your proposed level of means-assessment: anything from 0% to 100%… or beyond, but that does have some interesting philosophical consequences.

Then, on the “Expenses” sheet, record each thing that your household pays for over the course of each month. At the bottom, it’ll total up how much each person has paid, and how much they would have been expected to pay, based on the level of your means-assessment: at 0%, for example, each person would be expected to pay 1/N of the total; at the other extreme (100%), a person with no income would be expected to make no contribution, and a person with twice the income of another would be expected to pay twice as much as them. It’ll also show the difference between the two values: so those who’ve paid less than their ‘share’ will have negative numbers and will owe money to those who’ve paid more than their share, indicated by positive numbers. Settle the difference… and you’re ready to roll on to the next month.

Now you’re equipped to employ a (wholly or partially) means-assessed model to your household finances. If you adapt this model or have ideas for its future development, I’d love to hear them.

Uncommon Occurances

I didn’t sleep well; I woke up several times throughout the night. On the upside, I have a strong recollection of three distinct yet inter-related dreams:

Dream I: Alex and the Accident

I came into work as normal and spoke to Alex, my co-worker. He’d been in some sort of car accident in which he’d hit and killed a man in an electric scooter. There was a lot of ambiguity about whose fault it was – the man had apparently accelerated his scooter right out into traffic… but Alex had been driving too fast at the time.

Significance:

- My mum’s partner’s son, I recently learned, was in a car crash a week ago.

- At work yesterday my boss was telling me about expensive repairs to his car.

- I re-watched the shocking new don’t text and drive video yesterday.

Dream II – In The Red

I was a Western spy during the Cold War, attempting to infiltrate a Soviet University. With some difficulty, I was able to become enrolled at the University, but soon came under suspicion from the administrative management (all Party members, of course) after my luggage was found to contain a British newspaper. The newspaper contained details of Alex’s car crash, from Dream I, and this was later re-printed in the local newspapers, but with a suitably communist spin.

Later, after my cover was blown, I made plans to flee the country and return to the West.

Significance:

- Second dream references the first dream.

- The University campus was familiar; it was a little reminiscent of the University Of Worcester campus where I was at BiCon almost three weeks ago.

Dream III – Going To Work

I woke up, got dressed, and went to work. I discussed with co-workers Alex and Gareth a dream I’d had the previous night, in which Alex had crashed his car (as per Dream I) and about a film I’d seen the previous evening, about the infiltration of a Soviet University by a Western agent (as per Dream II). I explained that apparently the film was supposed to be about drugs, but maybe I’d failed to understand it because I didn’t see how it was supposed to be about drugs at all.

A client of ours paid a deposit on a reasonably-large job we’d quoted for, and I begun laying the foundations of the work as described in our technical specification.

Significance:

- Third dream references the first two dreams, but as different media: one as a dream, the other as a film!

- I’m expecting to get started on a new contract within the next couple of weeks, similar to the one referenced by the dream.

It was quite disappointing to be woken by my alarm and to discover that I still had to get up and go to work. While I’m usually quite aware that I’m dreaming when I’m dreaming, I somehow got suckered in by Dream III and had really got into the groove of going to work and getting on with my day, probably because I’d so readily assumed that Dream I was the dream and therefore that the same mundane things happening again must have been real life.

I was prompted to wonder, momentarily, if I might still be dreaming, when an unusual thing happened on the way to work. Just after I passed the site of the old post office sorting yard, about a third of the way to the office, I came across a woman crouched in a doorway, reaching out to a blue tit which was sat quite still in the middle of the pavement. Still half-asleep, I only barely noticed them in time to not walk right through them.

The bird must be injured, I thought, to not be flying away, as the woman managed to reach around it and pick it up. I stopped and waited to see if I could be of any use. Seconds later, the little creature wriggled free and flew off to perch on top of a nearby fence: it was perfectly fine!

The woman seemed as perplexed at this as I was: perhaps we both just found the world’s stupidest blue tit. I double-checked the clock on my phone (this is a reasonably-good “am I dreaming?” check for me, personally, as is re-reading text and using light switches) – but no, this was real. Just weird.

Edit: changed “Callbacks:” to “Significance:”. This is the format in which I’ll be blogging about the dreams I share with you now, I’ve decided.

Those Commie Martians

This story about the European Space Agency by the BBC reads:

…The Mars Exploration Rovers will touch down in January next year, just after the Europeans arrive with their Marx Express mission in December…

Marx Express? I suppose we should have guessed that the so-called ‘red planet’ was communist.