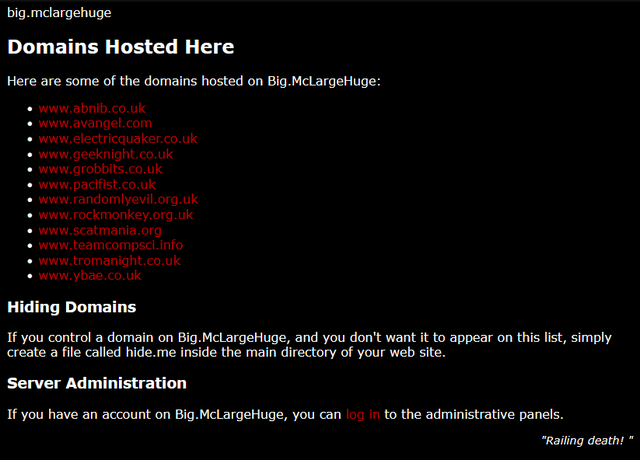

About twenty years ago, after a a tumultuouslife, Big.McLargeHuge – the shared server of several other Abnibbers and I – finally and fatally kicked the bucket. I spun up its replacement, New.McLargeHuge, on hosting company DreamHost, and this blog (and many other sites) moved over to it1.

Wow, I’d forgotten half of these websites existed.

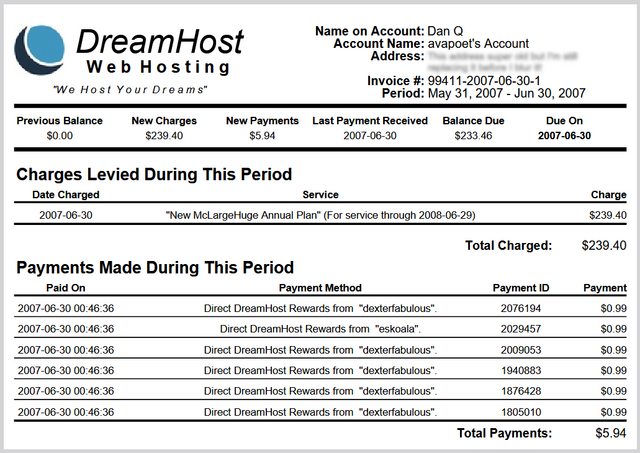

I only stayed with DreamHost for a few years before switching to Bytemark, with whom I was a loyal customer right up until a few years

ago2, but in that time I took advantage of DreamHost’s “Refer & Earn” program, which

allowed me to create referral codes that, if redeemed by others who went on to become paying customers, would siphon off a fraction of the profits as a “kickback” against my server

bills. Neat!3

DreamHost’s referrals had a certain “pyramid scheme” feel in that you could get credit for the people referred by the people you referred.

A year or so after I switched to ByteMark, DreamHost decided I owed them money: probably because of a

“quirk” in their systems. I disagreed with their analysis, so I ignored their request. They “suspended” my account (which I wasn’t using anyway), and that was the end of it.

Right?

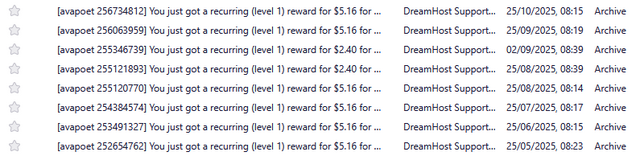

But the referral fees continued to trickle in. For the last seventeen years, I’ve received a monthly email advising me that my account had been credited, off the back of a

referral.

I have no explanation as to why the amount of the referral reward fluctuates, but I can only assume that it’s the result of different people on different payment schedules?

About once a year I log in and check the balance. I was quite excited to discover that, at current rates, they’d consider me “paid-up” for my (alleged) debt by around Spring 2026!

I had this whole plan that I’d write a blog post about it when the time came. It could’ve been funny!

But it’s not to be: DreamHost emailed me last night to tell me that they’re killing their “Refer & Earn” program; replacing it with something different-but-incompatible (social media’s

already having a grumble about this, I gather).

So I guess this is the only blog post you’ll get about “that time DreamHost decided I owed them money and I opted to pay them back in my referral fees over the course of eighteen

years”.

No big loss.

Footnotes

1 At about the same time I moved Three

Rings over from its previous host, Easily, to DreamHost too, in order to minimise the number of systems I had to keep an eye on. Oh, how different things are now, when I’ve

got servers and domain registrations and DNS providers all over the damn place!

2 Bytemark have rapidly gone downhill since their acquisition by Iomart a while back, IMHO.

3 Nowadays, this blog (and several of my other projects) is hosted by Linode, whose acquisition by Akamai seems not to have caused any problems with, so that’s fab.

Today, for the first time ever, I simultaneously published a piece of content across five different media: a Weblog post, a video essay, a podcast episode, a Gemlog post, and a

Spartanlog post.

Must be about something important, right?

Nope, it’s a meandering journey to coming up with a design for a £5 coin that will never exist. Delightfully pointless. Being the Internet I want to see in the world.

This post is also available as a video. If you'd prefer to watch/listen to me

talk about this topic, give it a look.

1979

The novelisation of The Hitch-Hiker’s Guide to the Galaxy came out in 1979, just a smidge before I was born. There’s a well-known scene in the second chapter featuring Ford

Prefect, an alien living on Earth, distracting his human friend Arthur Dent. Arthur is concerned about the imminent demolition of his house by a wrecking crew, and Ford takes him

to the pub to get him drunk, in anticipation of the pair attempting to hitch a lift on an orbiting spacecraft that’s about to destroy the planet:

“Six pints of bitter,” said Ford Prefect to the barman of the Horse and Groom. “And quickly please, the world’s about to end.”

The barman of the Horse and Groom didn’t deserve this sort of treatment, he was a dignified old man. He pushed his glasses up his nose and blinked at Ford Prefect. Ford ignored him

and stared out of the window, so the barman looked instead at Arthur who shrugged helplessly and said nothing.

So the barman said, “Oh yes sir? Nice weather for it,” and started pulling pints.

He tried again.

“Going to watch the match this afternoon then?”

Ford glanced round at him.

“No, no point,” he said, and looked back out of the window.

“What’s that, foregone conclusion then you reckon sir?” said the barman. “Arsenal without a chance?”

“No, no,” said Ford, “it’s just that the world’s about to end.”

“Oh yes sir, so you said,” said the barman, looking over his glasses this time at Arthur. “Lucky escape for Arsenal if it did.”

Ford looked back at him, genuinely surprised.

“No, not really,” he said. He frowned.

The barman breathed in heavily. “There you are sir, six pints,” he said.

Arthur smiled at him wanly and shrugged again. He turned and smiled wanly at the rest of the pub just in case any of them had heard what was going on.

None of them had, and none of them could understand what he was smiling at them for.

A man sitting next to Ford at the bar looked at the two men, looked at the six pints, did a swift burst of mental arithmetic, arrived at an answer he liked and grinned a stupid

hopeful grin at them.

“Get off,” said Ford, “They’re ours,” giving him a look that would have an Algolian Suntiger get on with what it was doing.

Ford slapped a five-pound note on the bar. He said, “Keep the change.”

“What, from a fiver? Thank you sir.”

There’s a few great jokes there, but I’m interested in the final line. Ford buys six pints of bitter, pays with a five-pound note, and says “keep the change”, which surprises the

barman. Presumably this is as a result of Ford’s perceived generosity… though of course what’s really happening is that Ford has no use for Earth money any longer; this point is

hammered home for the barman and nearby patrons when Ford later buys four packets of peanuts, also asking the barman to keep the change from a fiver.

Beer’s important, but you also need to know where your towel is.

We’re never told exactly what the barman would have charged Ford. But looking at the history of average UK beer prices and assuming that the story is set in 1979, we can

assume that the pints will have been around 34p each1,

so around £2.04 for six of them. So… Ford left a 194% tip for the beer2.

1990

By the time I first read Hitch-Hikers, around 1990, this joke was already dated. By then, an average pint of bitter would set you back £1.10. I didn’t have a good

awareness of that, being as I was well-underage to be buying myself alcohol! But I clearly had enough of an awareness that my dad took the time to explain the joke… that is, to point

out that when the story was written (and is presumably set), six pints would cost less than half of five pounds.

But by the mid-nineties, when I’d found a friend group who were also familiar with the Hitch-Hikers… series, we’d joke about it. Like pointing out that by then if

you told the barman to keep the change from £5 after buying six pints, the reason he’d express surprise wouldn’t be because you’d overpaid…

In his defence, Ford’s an alien and might not fully understand human concepts of inflation. Or sarcasm.

1998

Precocious drinker that I was, by the late nineties I was quite aware of the (financial) cost of drinking.

Sure, this seems like a responsible amount of alcohol for a party thrown by a couple of tearaway teenagers. Definitely nothing going to go wrong here, no siree.

And so when it was announced that a new denomination of coin – the £2 coin –

would enter general circulation3

I was pleased to announce how sporting it was of the government to release a “beer token”.

With the average pint of beer at the time costing around £1.90 and a still cash-dominated economy, the “beer token” was perfect! And in my case, it lasted: the bars I was

drinking at in the late 1990s were in the impoverished North, and were soon replaced with studenty bars on the West coast of Wales, both of which allowed the price of a pint to do

battle with inflationary forces for longer than might have been expected elsewhere in the country. The “beer token” that was the £2 coin was a joke that kept on giving for some time.

The one thing I always hated about the initial design for the bimetallic £2 coin was – and this is the nerdiest thing in the world with which to take issue – the fact that it had a

ring of 19 cogs to represent British industry. But if you connect a circuit of an odd number of cogs… it won’t function. Great metaphor, there. Photo

courtesy of the late Andy Fogg, used under a Creative Commons license.

2023

As the cost of living rapidly increased circa 2023, the average price of a pint of beer in the UK finally got to the point where, rounded to the nearest whole pound, it was closer to £5

than it is to £44.

And while we could moan and complain about how much things cost nowadays, I’d prefer to see this as an opportunity. An opportunity for a new beer token: a general-release

of the £5 coin. We already some defined characteristics that fit: a large,

heavy coin, about twice the weight of the £2 coin, with a copper/nickel lustre and struck from engravings with thick, clear lines.

And the design basically comes up with itself. I give you… the Beer Token of the 2020s:

Wouldn’t this be much more-satisfying to give to a barman than a plasticky note or a wave of a contactless card or device?

It’s time for the beer token to return, in the form of the £5 coin. Now is the time… now is the last time, probably… before cash becomes such a rarity that little thought

is evermore given to the intersection of its design and utility. And compared to a coin that celebrates industry while simultaneously representing a disfunctional machine, this is a

coin that Brits could actually be proud of. It’s a coin that tourists would love to take home with them, creating a satisfying new level of demand for the sinking British

Pound that might, just might, prop up the economy a little, just as here at home they support those who prop up the bar.

I know there must be a politician out there who’s ready to stand up and call for this new coin. My only fear is that it’s Nigel Fucking Farage… at which point I’d be morally compelled

to reject my own proposal.

But for now, I think I’ll have another drink.

Footnotes

1 The recession of the 1970s brought high inflation that caused the price of beer to

rocket, pretty much tripling in price over the course of the decade. Probably Douglas Adams didn’t anticipate that it’d more-than-double again over the course of the 1980s

before finally slowing down somewhat… at least until tax

changes in 2003 and the aftermath of the 2022 inflation rate spike!

2 We do know that the four packets of peanuts Ford bought later were priced at 7p

each, so his tip on that transaction was a massive 1,686%: little wonder the barman suddenly started taking more-seriously Ford’s claims about the imminent end of the world!

3 There were commemorative £2 coins of a monometallic design floating around already, of

course, but – being collectible – these weren’t usually found in circulation, so I’m ignoring them.

4 Otherwise known as “two beer tokens”, of course. As in “Bloody hell, 2022, why does a

pint of draught cost two beer tokens now?”

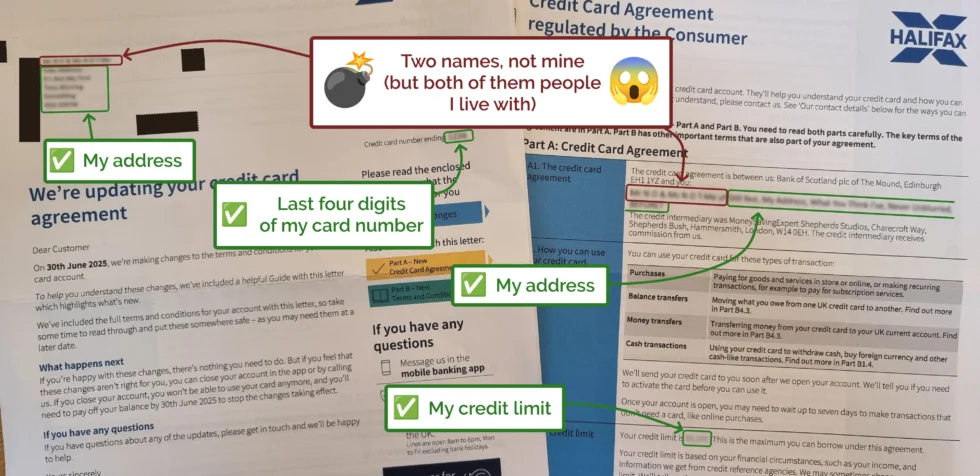

Today, Ruth and JTA received a letter. It told them about an upcoming change to the

agreement of their (shared, presumably) Halifax credit card.

Except… they don’t have a shared Halifax credit card. Could it be a scam? Some sort of phishing attempt, maybe, or perhaps somebody taking out a credit card in their names?

I happened to be in earshot and asked to take a look at the letter, and was surprised to discover that all of the other details – the last four digits of the card, the credit

limit, etc. – all matched my Halifax credit card.

Halifax sent a letter to me, about my credit card… but addressed it to… two other people I live with‽

I spent a little over half an hour on the phone with Halifax, speaking to two different advisors, who couldn’t fathom what had happened or how. My credit card is not (and has never

been) a joint credit card, and the only financial connection I have to Ruth and JTA is that I share a mortgage with them. My guess is that some person or computer at Halifax tried to

join-the-dots from the mortgage outwards and re-assigned my credit card to them, instead?

Eventually I had to leave to run an errand, so I gave up on the phone call and raised a complaint with Halifax in writing. They’ve promised to respond within… eight weeks. Just

brilliant.

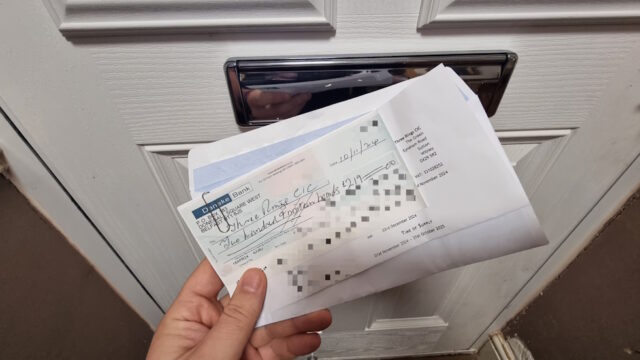

My Three Rings volunteering this International Volunteer Day isn’t all technical work. It’s also time to process the incoming postal mail.

Our time as volunteers may be free, but our servers aren’t, so the larger and richer charities that use our services help contribute to our hosting costs. Most send money digitally, but

some use dual-signatory accounts that require they send cheques.

eBay UK have changed their terms to (a) remove seller fees for most private sellers, but (b)

instead of paying-out immediately, payouts are four times a year (or on-demand).

That sounds like they’re trying to keep money in their ecosystem. The hope is, I guess, that by paying sellers in virtual “eBay Pounds” rather than actual money in the first instance

they’ll encourage those sellers to become buyers again (either of other listings, or of eBay’s postage and other services). You can cash out anytime you like, but you can never leave.

You see the same technique used e.g. by the National Lottery, who pay out “small” winnings into your online account, knowing that the vast majority of winnings are on the order of only

a few times more than the value of a ticket, and so players will be more-likely to “re-invest” if they’re not paid-out directly.

It became clear a good chunk of my Automattic colleagues disagreed with me and our actions.

So we decided to design the most generous buy-out package possible, we called it an Alignment Offer: if you resigned before 20:00 UTC on Thursday, October 3, 2024, you would receive

$30,000 or six months of salary, whichever is higher.

…

HR added some extra details to sweeten the deal; we wanted to make it as enticing as possible.

I’ve been asking people to vote with their wallet a lot recently, and this is another example!

…

This was a really bold move, and gave many people I know pause for consideration. “Quit today, and we’ll pay you six months salary,” could be a pretty high-value deal for some people,

and it was offered basically without further restriction2.

Every so often, though, I spend time with a company that is so original in its strategy, so determined in its execution, and so transparent in its thinking, that it makes my head

spin. Zappos is one of those companies

…

It’s a hard job, answering phones and talking to customers for hours at a time. So when Zappos hires new employees, it provides a four-week training period that immerses them in the

company’s strategy, culture, and obsession with customers. People get paid their full salary during this period.

After a week or so in this immersive experience, though, it’s time for what Zappos calls “The Offer.” The fast-growing company, which works hard to recruit people

to join, says to its newest employees: “If you quit today, we will pay you for the amount of time you’ve worked, plus we will offer you a $1,000 bonus.” Zappos actually bribes its

new employees to quit!

…

I’m sure you can see the parallel. What Zappos do routinely and Automattic did this week have a similar outcome

By reducing – not quite removing – the financial incentive to remain, they aim to filter their employees down to only those whose reason for being there is that they

believe in what the company does3. They’re trading money for

idealism.

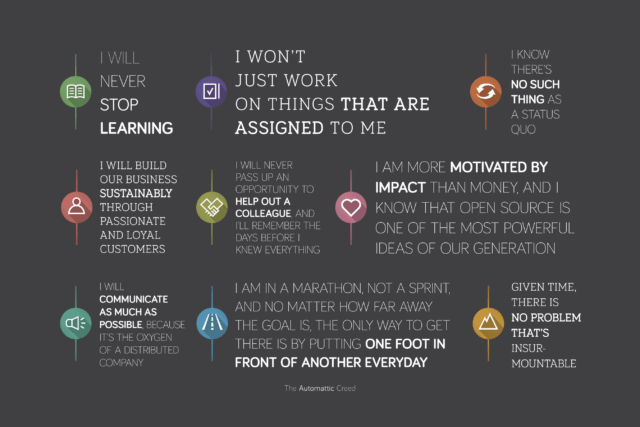

Buried about half way through the Creed is the line I am more motivated by impact than money, which seems

quite fitting. Automattic has always been an idealistic company. This filtering effort helps validate that.

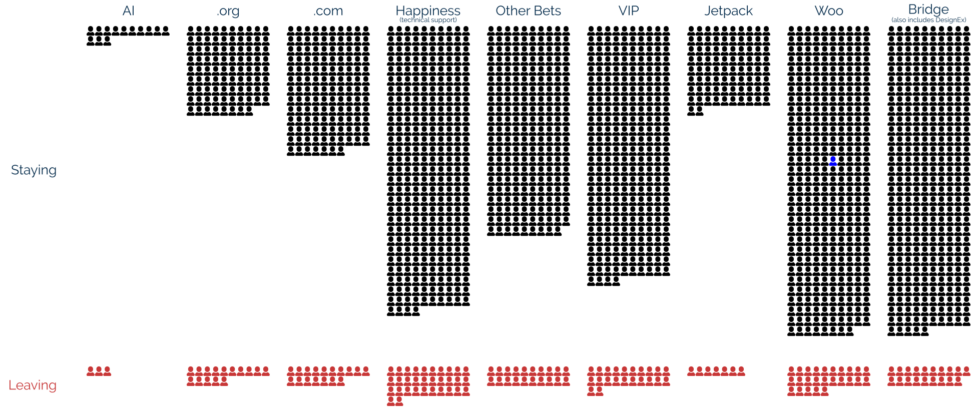

The effect of Automattic’s “if you don’t feel aligned with us, we’ll pay you to leave” offer has been significant: around 159 people – 8.4% of the company – resigned this week. At very

short notice, dozens of people I know and have worked with… disappeared from my immediate radar. It’s been… a lot.

I chose to stay. I still believe in Automattic’s mission, and I love my work and the people I do it with. But man… it makes you second-guess yourself when people you know, and respect,

and love, and agree with on so many things decide to take a deal like this and… quit4.

Departures have been experienced across virtually all divisions, but not always proportionally.

(These numbers are my own estimation and might not be entirely accurate.)

There’ve been some real heart-in-throat moments. A close colleague of mine started a message in a way that made me briefly panic that this was a goodbye, and it took until half way

through that I realised it was the opposite and I was able to start breathing again.

But I’m hopeful and optimistic that we’ll find our feet, rally our teams, win our battles, and redouble our efforts to make the Web a better place, democratise publishing (and

eCommerce!), and do it all with a commitment to open source. There’s tears today, but someday there’ll be happiness again.

Footnotes

1 For which the Internet quickly made me regret my choices, delivering a barrage of

personal attacks and straw man arguments, but I was grateful for the people who engaged in meaningful discourse.

2 For example, you could even opt to take the deal if you were on a performance

improvement plan, or if you were in your first week of work! If use these examples because I’m pretty confident that both of them occurred.

3 Of course, such a strategy can never be 100% effective, because people’s reasons for

remaining with an employer are as diverse as people are.

4 Of course their reasons for leaving are as diverse and multifaceted as others’ reasons

for staying might be! I’ve a colleague who spent some time mulling it over not because he isn’t happy working here but because he was close to retirement, for example.

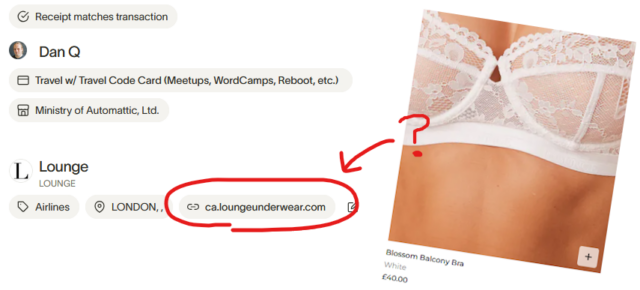

At work, we recently switched expenses system to one with virtual credit card functionality. I decided to test it out by buying myself lounge access for my upcoming work trip to Mexico.

Unfortunately the new system mis-detected my lounge access as being a purchase from lingerie company loungeunderwear.com. I’m expecting a ping

from Finance any moment to ask me why I’m using a company credit card to buy a bra.

One might ask why our expenses provider can (mis-)identify loungeunderwear.com from a transaction in the first place. Did somebody at some company that uses this provider

actually buy some ladies’ briefs on a company credit card at some point?

But if I ever happen to be somewhere that the lottery results are being announced, I sometimes like to play a game I call Not The Lottery.2

Here’s how you play:

Set aside the money it would have cost for a ticket.

Think of the numbers you’d have played.

When those numbers don’t come up, congratulations: you just won not-wasting-your-money!3

Want to play Not The Lottery retroactively? Cool. I’ve made and open-sourced a tool for that. Hopefully it’ll load below

and you can choose some numbers (or take a Lucky Dip) and have it played through the entirety of EuroMillions history and see how much money you’d have won if you’d only played them

every week. Or, to look at things from a brighter perspective, how much you’ve saved by not playing. It’s almost-certainly in the thousands.

Loading game… please wait… (if it

never loads, Dan probably broke it; sorry!)

Winning the lottery

But that’s not what the question’s really about, is it? We don’t ask people “what would they do if they won the lottery?” because we think it’s likely to happen4

We ask them because… well, because it’s fun to fantasise.

And I sort-of gave the answer away on day 20 of Bloganuary: I’d do my “dream job”. I’d work (for free) for Three Rings, like I already do, except instead of spending a couple of hours a week on it on average I’d spend about ten times that. I’d use the

luxury of not having to work to focus on things that I know I can do to make the world a better place.

If money was no object, I’d spend more time with these happy folks (and many more besides), making volunteering easier for everybody.

Sure, there’s other things I’d do. They’re mostly obvious things that I’d hope anybody in my position would do. Pay off the mortgage (and for all the works currently being done to

infuriate the dog improve the house). Arrange some kind of slow-access trust or annuity for the people closest to me so that

they need not worry about money, nor about having to work out how to spend, save, or invest a lump sum. Maybe a holiday or two. Certainly some charitable donations. Perhaps buy

really expensive ketchup: the finest dijon ketchup5.

But mostly I’d just want to be able to live as comfortably as I do now, or perhaps slightly more, and spend a greater proportion of my time than I already do making charities work

better.

I don’t know if that makes me insufferably self-righteous or insufferably simple-minded, but it’s probably one of those.

Footnotes

1 I’ve been caught describing it as “a tax on people who are bad at maths”, but I don’t

truly believe that (although I am concerned about how readily we let people get addicted to problematic gambling and then keep encouraging them to play with dark patterns that hide

how low the odds truly are). I’ve even been known to buy a ticket or two, some years.

2 While writing this, I decided to retroactively play for last Friday, having not seen

whatever numbers came up. I guessed only one of them. Hurrah! That means I saved £2.50 by not playing!

3 There are, of course, other possible outcomes. You could have missed out on winning a

small prize – the odds aren’t that low – but the solution to this is simple: just keep playing Not The Lottery and you, as the “house”, will come out on top in the end.

Alternatively, it’s just-about possible that you could pluck the jackpot numbers from thin air, in which case: well done! You’re doing better than Derren Brown when in 2009 he

performed a pretty good magic trick but then turned it into a turd when he

“explained” it using pseudoscience (why not just stick with “I’m a magician, duh”; when you play the Uri Geller card you just make yourself look like an idiot). Let’s find a way

to use those superpowers for good. Because what you’ve got is a superpower. For context: if you played Not The Lottery twice a week, every week, without fail, for

393 years… you’d still only have a 1% chance of having ever predicted a jackpot in your five-lifetimes.

4 What if we lived in a world where we did use statistics to think about the

hypothetical questions we ask people? Would we ask “what would you do if you were stuck by lightning?”, given that the lifetime chance of being killed by lightning is significantly

greater than the chance of winning the jackpot, even if you play every draw!

Of course, you don’t strictly need a digital wallet to use EGX. But as we’re in a culture where people invariably ask “is

there an app for it?”, I thought I’d make one.

You can install it as an offline-first progressive web application, which means that this could be the first ever digital currency to have an app that works without an Internet

connection. That’s probably something no other digital currency can claim to have, right?

Here’s what it looks like if I send 0.1 EGX to my friend Chris using the app:

Naturally, I wouldn’t be backing Emma Goldcoin if it didn’t represent such a brilliant step up better-known digital currencies like Bitcoin, Ripple, and Etherium. Specific features

unique to Emma Goldcoin include:

Using it doesn’t massively contribute to energy wastage and environmental damage.

It doesn’t increase the digital divide by helping early adopters at the expense of late adopters.

It’s entirely secure: it’s mathematically impossible to “steal”EGX.

Emma Goldcoin is so simple that you don’t even need a computer to use it: it “just works”.

Sure, it’s got its downsides, and I’d encourage you to read the specification if you’d like to learn more about what

those are. Or if you already know what EGX is all about and just want to try a new way to manage your portfolio, give my new site EGXchange.org a go!

£20 for a boiled egg, one piece of toast and a mug of tea?

The story of a modern London cafe…

(Read to end of thread before commenting!)

…

An amazing thread well-worth reading to the end. Went in expecting a joke about hipsters, millennials, and avocado-on-toast… finished with something much more.

The web’s founders fully expected some form of digital payment to be integral to its functioning. But nearly three decades later, we’re still waiting.

Back in the 1990s, when Tim Berners-Lee and his team were creating the infrastructure of the World Wide Web, they made a list of the error codes that would

pop up when something went wrong. You’ve surely encountered many of them: “404 Not Found,”

which pops up if you click on a dead link; “401 Unauthorized” when you hit a page that needs a password; and so on.

Here’s one you probably haven’t seen—and its absence from your life speaks to why the promise of the early web seems increasingly out of reach: “402 Payment Required.”

That’s right: The web’s founders fully expected some form of digital payment to be integral to its functioning, just as

integral as links, web pages, and passwords. After all, without a way to quickly and smoothly exchange money, how would a new economy be able to flourish online? Of course there ought

to be a way to integrate digital cash into browsing and other activities. Of course.

Yet after almost three decades, that 402 error code is still “reserved for future use.” So I still have to ask: Where are my digital micropayments? Where are those frictionless,

integrated ways of exchanging money online—cryptographically protected to allow commerce but not surveillance?

…

In response to this article being discussed on MetaFilter, I wrote:

The Web Payments Working Group published a specification for a standardised mechanism for the collection of card payment details online,

a couple of years ago. It’s not quite the same thing because it’s done in the page application rather than at the HTTP(S) level, but it goes a long way towards solving a lot of the

problems with our existing approach to payment processing online.

It’s already seeing adoption in browsers, but merchants and payment processors are unlikely to start rolling it out until adoption until later because (a) they want critical mass and

(b) they’re wary of change. But within a few years, you’ll probably see it for the first time, and you might not even notice.

The idea is that instead of asking you to fill out an (arbitrary) form, a web page will ask your browser to get payment details from you in a standardised format. That might

mean entering your card details if that’s how you prefer to work (but even if you choose to do this, the form you fill in will look the same every time) but it would instead allow you

to use a payment tool built in to your browser, operating system, or password safe to do it for you. I know that browsers and password safes will offer to try to do this

today, but standardising the format means that they’ll always be able to achieve it.

Once this technology’s in place, there’s nothing to stop HTTP 402’s implementation being completed: all the infrastructure will exist.

The thing about the future is that when it arrives, you don’t even notice. It’s never jetpacks and flying cars: it’s a series of iterative changes, each one predictable after the

completion of the last but the entire ensemble seeming innovative and surprising when taken as a whole.

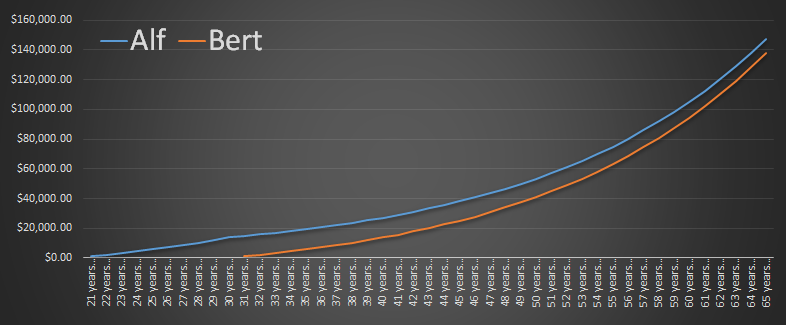

Spectacular example of why when saving (e.g. for a pension) it’s often more important to save early than it is to save lots. So get saving! Even with an understanding

of compound interest, these numbers can surprise you.

The only time better than today would have been yesterday, and you already missed that boat.